Key takeaways

- ITIN is required for non-resident LLC owners only when they need to file a US tax return, claim a tax treaty benefit, or receive certain types of income.

- A Certifying Acceptance Agent (CAA) lets foreign founders complete the W-7 application without mailing original passport documents to the IRS.

- Processing time runs 7-14 weeks; do not send a notarized copy from a US notary, the IRS rejects them.

Before you start

- Confirm you actually need an ITIN; foreign-owned single-member LLCs with no US-source income usually do not.

- Locate a Certifying Acceptance Agent in your country if you want to avoid mailing original documents.

Who this is for

- Non-resident foreign founders forming a US LLC.

- Multi-member LLC owners with at least one non-resident member required to file a US return.

An Individual Taxpayer Identification Number (ITIN) is a US tax processing number issued by the IRS to individuals who need to file or be reported on a US tax return but are not eligible for a Social Security Number (SSN). For non-resident LLC owners, the ITIN is the personal tax ID that the EIN cannot replace.

The most common confusion at the start of a foreign-founded LLC is treating the ITIN and the EIN as alternates. They are not. The Employer Identification Number (EIN) belongs to the LLC as a business entity. The ITIN belongs to the human individual filing taxes, claiming a treaty benefit, or being listed as a beneficial owner. Almost every foreign LLC owner needs both, just at different points in the company's first 1-3 years.

This guide separates the cases where an ITIN is genuinely required from the cases where founders apply for one prematurely, the most common mistake. It walks through Form W-7, the certified document path, the 7-14 week IRS timeline, and the Certifying Acceptance Agent (CAA) shortcut that compresses that timeline. Foreign founders who paid for a CAA service and still waited 12 weeks usually skipped one of the four signoff steps below.

Setting up your LLC? See your US address options — no card →

ITIN vs EIN: two different numbers, two different purposes

The IRS issues four different identifying numbers. Two of them apply to entities (EIN, taxpayer reference for trusts), and two apply to individuals (SSN for US persons, ITIN for non-US persons filing US tax returns). Confusion between EIN and ITIN is the single most expensive misstep on a foreign-founder LLC, since applying for the wrong one delays everything downstream.

| Number | Belongs to | Purpose | Issued by | When you need it |

|---|---|---|---|---|

| EIN | The LLC entity | Business tax filings, banking, payroll, BOI | IRS | Right after LLC formation, before opening any bank account |

| ITIN | The individual owner | Personal tax filings, tax treaty, banking ID for some institutions | IRS | When you receive US-source income that has to be reported on a 1040-NR |

| SSN | US persons only | Personal tax, employment, Social Security benefits | Social Security Administration | Not available to non-US persons unless authorized to work in US |

EIN, ITIN, and SSN compared. Foreign LLC owners typically need the EIN first (for the LLC) and the ITIN later (for personal tax filings).

In practice, the EIN comes first, since the LLC needs it to open a bank account, accept payments, and file the BOI report. The ITIN comes later, only when the IRS or a counterparty needs to identify the human owner separately from the LLC. Many foreign founders go an entire first year without an ITIN because the LLC is not yet generating US-source income that flows to the owner's individual return.

When you actually need an ITIN

The ITIN is event-triggered, not a default formation step. The five situations below cover the cases where a non-resident LLC owner has to apply.

- Filing Form 1040-NR. The non-resident individual income tax return. Required when the LLC is taxed as a partnership that issues a Schedule K-1 to a non-resident member, or when the LLC pays out fixed, determinable, annual, or periodic (FDAP) income to the owner. (Note: nonresident aliens cannot be direct S-corporation shareholders under IRC §1361(b)(1)(C); they may only hold S-corp shares indirectly through an Electing Small Business Trust.)

- Claiming a tax treaty benefit. If the home country has a US tax treaty (UK, Germany, India, South Korea, Japan, Canada, and 60+ others), the ITIN is required to claim reduced withholding on US-source income. Without an ITIN, the default 30% withholding applies even when the treaty rate is 5-15%.

- Form 5472 reporting for foreign-owned single-member LLCs. When a non-resident owns a single-member US LLC, the LLC files a pro forma Form 1120 plus Form 5472 every year. The ITIN of the foreign owner goes on the 5472 as the reportable transaction party, even though the LLC itself uses the EIN.

- Receiving 1099-NEC, 1099-MISC, or 1099-K as an individual contractor. If a US client treats the foreign founder as an individual contractor, the 1099 reporting requires an ITIN. This is rare for properly structured LLCs but common in early-stage one-person businesses that invoice in the founder's name.

- Personal investment account at a US brokerage. Charles Schwab International, Interactive Brokers, and Fidelity International accept the ITIN as a US tax ID for opening a personal investment account. Most fintechs that serve LLCs (Mercury, Wise, Brex) do not require the owner's ITIN for the LLC business account.

What an ITIN is *not* needed for: applying for an EIN. The companion guide on getting an EIN without an SSN walks through the Form SS-4 fax path that bypasses the ITIN requirement entirely. Applying for an ITIN first to then apply for an EIN adds 8-14 weeks to a process that can finish in 4-6 weeks via the fax path.

Ready to set up your business address?

See which US cities fit — about a minute, no card needed.

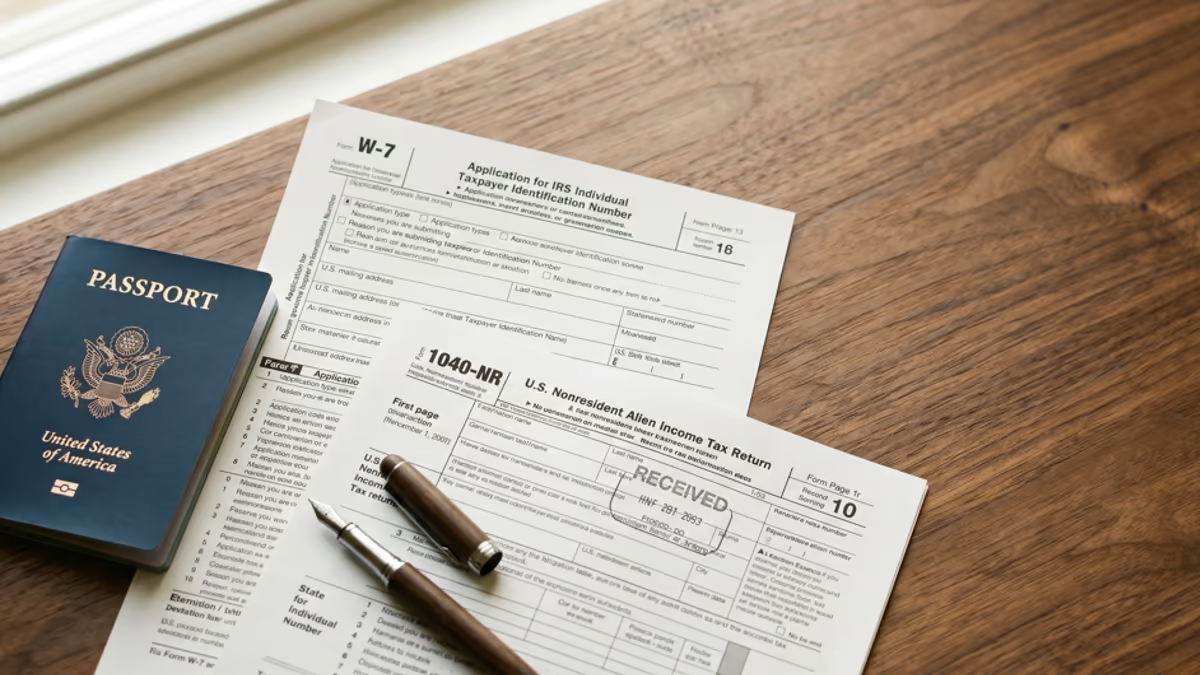

The Form W-7 application process

Form W-7 is the application for an ITIN. The form itself is short, one page with six sections, but the supporting documentation is what determines whether the application succeeds the first time. Most ITIN rejections are document defects, not form defects.

- 1Reason for applying. Sections (a) through (h) of the form. The most common boxes for non-resident LLC owners are box (b) 'Nonresident alien filing a US tax return', box (h) 'Other' with treaty benefit reason, or box (a) 'Nonresident alien required to get ITIN to claim tax treaty benefit'.

- 2Personal information. Full name, date of birth, country of citizenship, foreign tax ID if any, US visa number if any. The name has to match the passport exactly: no nicknames, no shortened middle names, no Latin transliteration that drops accents.

- 3US tax return attachment. The W-7 is filed *together with* the tax return that requires it (usually Form 1040-NR), not separately. Filing W-7 alone without the underlying tax return is the second most common rejection reason.

- 4Supporting documentation. Original passport or certified copy from the issuing authority, plus one of three secondary documents (national ID, foreign driver's license, or US visa) if the passport alone is not sufficient.

- 5Mail or in-person submission. Mail the W-7 plus tax return plus supporting documents to the IRS ITIN unit at Austin, Texas. Or present in person at an IRS Taxpayer Assistance Center. Or submit through a Certifying Acceptance Agent, covered in the next section.

Documents that pass: passport, country ID, and certified copies

The IRS accepts 13 specific documents to verify identity and foreign status. The single document that does both is a passport. The 12 alternate documents come in pairs: one to prove identity, one to prove foreign status. Most foreign founders use the passport route.

- Passport (single document option). The simplest path. The original passport, mailed to the IRS, is returned within 60 days. Or a copy certified by the issuing country's authority, the foreign Ministry of Foreign Affairs or US embassy in the home country.

- Two-document combination (alternate path). Identity document (national ID card, US driver's license, or foreign driver's license with photo) plus foreign status document (foreign birth certificate, foreign voter registration card, or US visa).

- Certified copy from issuing authority is the safest path that does not require mailing the original passport. The certification has to come from the agency that issued the passport, not a notary public or a lawyer.

- Photocopies notarized at a US notary public are not accepted. This is the most common document rejection. US notaries do not have authority to certify foreign documents, even when the notarial seal looks official.

Do not send a notarized copy from a US notary

A notarized copy of a foreign passport from a US notary is rejected nearly 100% of the time. The IRS specifically requires either the original document, a certified copy from the foreign issuing authority, or processing through a Certifying Acceptance Agent. Plan for either mailing the original passport or scheduling a CAA appointment.

The CAA (Certifying Acceptance Agent) shortcut

A Certifying Acceptance Agent (CAA) is a person or firm that has signed a formal agreement with the IRS to verify ITIN applicant documents in person and forward only the application to the IRS. The CAA handles the document verification step that would otherwise require mailing the original passport. For most foreign founders, the CAA route is what makes ITIN application practical.

CAAs are listed on the IRS website at irs.gov under the acceptance agent program. The list is global, with CAAs in the UK, Canada, India, Mexico, Brazil, and most major US-business jurisdictions. CAA fees typically run $150-400 for the document verification, with most CAAs requiring an in-person or video appointment to physically inspect the passport.

- 1Find a CAA in the home country or in the destination US city through the IRS list.

- 2Book the appointment in person or via secure video. Some CAAs accept video for non-US-resident applicants under specific procedures that the IRS authorized for international applicants.

- 3Bring the passport, the completed Form W-7, and the underlying tax return (Form 1040-NR with all schedules and supporting documents).

- 4The CAA verifies the passport, signs Form W-7 as the agent, and forwards only the W-7 plus tax return to the IRS Austin office. The original passport stays with the applicant.

- 5The IRS processes within 7-11 weeks for standard, extending to 14 weeks during peak tax season (January-April), the same window as direct application, but without the passport in transit and with meaningfully better acceptance odds — IRS Taxpayer Advocate Service (2024 Annual Report) reports CAA-routed applicants are 15% more likely to be accepted, and direct-mail applicants are more than twice as likely to be rejected.

Timeline, renewal, and what 'expired' means

The IRS quotes a 7-14 week processing window for ITIN applications. In practice, the window depends heavily on filing season. Applications filed January through April 15, the peak tax season, often run the full 14 weeks or longer. Applications filed May through November typically clear in 7-9 weeks.

- Initial issuance: 7-14 weeks from the IRS receipt date.

- Renewal triggers: ITINs not used on a US tax return for 3 consecutive years expire and have to be renewed. The IRS also runs scheduled renewal cycles where ITINs in certain ranges have had to be renewed even when used.

- What happens if expired: A tax return filed with an expired ITIN is processed but the related deductions, credits, and refunds are denied until the ITIN is renewed.

- Renewal application: Form W-7 again, marked as renewal in section (a), with the same supporting documents. Renewal takes 7-11 weeks.

Foreign founders who use their ITIN every year on Form 1040-NR or Form 5472 do not hit the 3-year non-use trigger. Founders who applied for an ITIN once for a treaty benefit on a single-year transaction and then went silent are the most common renewal cohort.

ITIN for US banking, brokerage, and investment accounts

Most US fintechs (Mercury, Relay, Brex, Wise) do not require the LLC owner to have an ITIN to open the LLC business account. The LLC's EIN is the tax ID the bank uses, not the owner's ITIN. The ITIN comes into play for personal accounts, investment brokerages, and a few specific situations.

- Personal investment accounts. Charles Schwab International, Interactive Brokers, and Fidelity International accept ITIN holders. The ITIN goes on Form W-8BEN, which triggers treaty-rate withholding on US-source dividends and capital gains.

- Joint accounts with a US-resident spouse. An ITIN-holding non-resident spouse can be added to a joint account with an SSN-holding US spouse. The ITIN goes on the 1099 reporting for the non-resident's share.

- US-based payment platforms like PayPal Personal: Some platforms accept ITIN-based personal accounts when the user is processing US-source income as an individual rather than through an entity. Most LLC operations use the LLC business account instead.

- Real estate transactions. ITIN required for the foreign individual on Form 1099-S when the real estate is held in the individual's name rather than the LLC's name.

For LLC banking specifically, the bank account address requirements guide covers what Mercury, Relay, and Bluevine actually verify (none of which is the ITIN). The Certificate of Good Standing guide covers the apostille step that often runs alongside ITIN application for foreign founders preparing international banking documents.

Common rejection reasons and how to recover

The IRS publishes the top rejection reasons in the W-7 instructions. The four below cover roughly 80% of rejections.

- Notarized copy of passport from a US notary instead of certified copy from issuing authority or original document. Fix: send the original passport, get a certified copy from the foreign authority, or use a CAA.

- W-7 filed alone without the underlying tax return. Fix: file W-7 together with Form 1040-NR or whichever return triggers the ITIN requirement, except for treaty benefit-only cases that are filed as standalone with supporting treaty documentation.

- Name on W-7 does not match passport exactly. Fix: use the passport name exactly, including all middle names and any hyphens or accents that appear on the passport.

- Reason for applying box not selected, or wrong box selected for the specific tax situation. Fix: review the W-7 instructions Section 5 carefully. The most common correct boxes for foreign LLC owners are (b), (h) with treaty reason, or (a) for treaty-only filings.

After a rejection, the recovery path is to fix the specific issue (often a single document or a single line on W-7) and resubmit with the original tax return attached. The 7-14 week timer restarts. CAA-routed applications have meaningfully better acceptance odds than direct mail (IRS Taxpayer Advocate Service reports CAA applicants are 15% more likely to be accepted; non-CAA applicants are more than 2x more likely to be rejected), primarily because the CAA catches document defects at the appointment before the application leaves the office.

Frequently Asked Questions

Not sure what you need?

Two short pages sort it out — what the products actually are, and which situation you're in.