Short answer

Under current FinCEN guidance, LLCs and corporations formed in a US state are exempt from beneficial ownership reporting, even when every owner lives abroad. The rule now points at foreign reporting companies, meaning entities formed under another country's law and registered to do business in the US. The rule has changed shape repeatedly, so check FinCEN's own BOI page before relying on any summary.

Key takeaways

- The Corporate Transparency Act's reporting rule has been rewritten repeatedly since 2024, which is why confident answers from last year are often wrong this year.

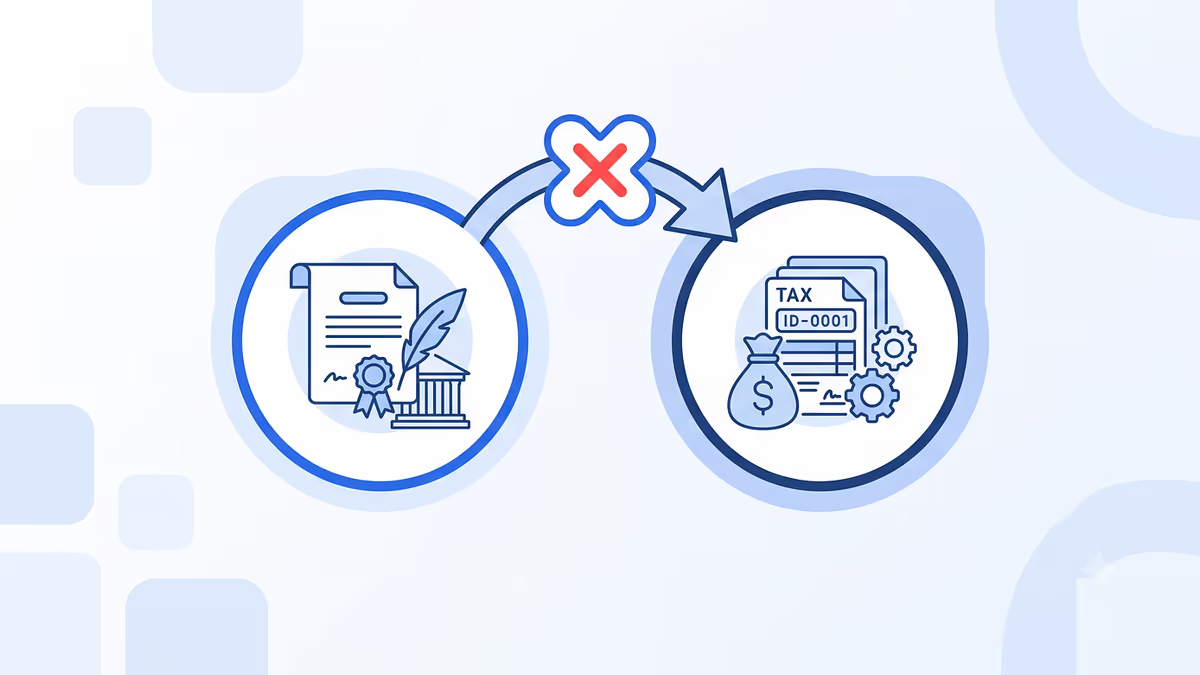

- In FinCEN's language, a foreign reporting company is an entity formed under another country's law, not a US company with foreign owners. A Delaware or Wyoming LLC is domestic no matter where its owners live.

- The exemption does not touch your other obligations: the EIN, the registered agent, Form 5472 for a foreign-owned single-member LLC, and state annual reports all still apply.

- If you filed a BOI report before the rule narrowed, a later exemption does not usually require you to withdraw a filing made in good faith.

Ask ten founders running a U.S. LLC whether they still need to file a beneficial ownership report this year, and you’ll get five different answers. At least two of them will be stated with total confidence and be wrong.

That’s not really their fault. It’s what happens when a federal rule gets rewritten three separate times in about eighteen months, while everyone downstream of it — a lawyer’s old blog post, a formation service’s FAQ page, a founder group chat from last spring — is still running on whichever version they happened to read first.

How the Rule Got Smaller

Quick recap, because the history explains the confusion. The Corporate Transparency Act asked millions of small companies to report their real owners to FinCEN starting in 2024. Courts blocked the requirement, then unblocked it, flipping within days of each other at one point. FinCEN pushed the deadline back more than once while that played out. Then, in a move that mattered a lot more than most compliance news does, FinCEN excused domestic companies and U.S. persons from the requirement altogether and pointed the rule at foreign reporting companies instead. The direction since has stayed consistent: fewer filers, less paperwork, narrower scope. That’s the policy shift sitting behind this week’s headlines too.

Here’s the part worth sitting with. The question that actually matters isn’t what the rule says. It’s how you find out what’s true on the day you’re reading this.

What Foreign Actually Means Here

The detail that trips up a lot of non-resident founders is the word foreign. In FinCEN’s language, a foreign reporting company isn’t a company with foreign owners. It’s a company formed under the law of another country that’s registered to do business in the U.S. A Delaware or Wyoming LLC is a domestic reporting company no matter who signed the operating agreement or where they live. Own a U.S. LLC from anywhere in the world, and the entity itself is still domestic under this rule. That single distinction is why a lot of non-resident owners who assumed they were squarely in scope have, under the current guidance, been let out of it.

Worth saying plainly, so nobody reads too much into this: it doesn’t touch your other obligations. An EIN, a registered agent, Form 5472 if you’re running a foreign-owned single-member LLC, your state’s annual report. Beneficial ownership reporting was one item on that list, and it happens to be the one getting lighter.

Ready to set up your business address?

See which US cities fit — about a minute, no card needed.

The Honest Limit of Any Answer Written Today

I’d normally tell you exactly where that leaves you. But that’s the honest limit of writing about this topic in the middle of 2026: whatever I say with certainty here has a real chance of being stale by the time you read it, because this rule has already changed shape more times than almost any other compliance requirement small businesses deal with. The useful move isn’t memorizing today’s answer. It’s building the habit of checking FinCEN’s own site directly, or asking whoever handles your filings, before assuming last year’s answer still holds.

That habit is really the whole story here. The BOI form itself was never the burden. It took most people twenty minutes and cost nothing to file through FinCEN’s own portal. The burden was the uncertainty: not knowing whether you were required to file, whether a court had paused it that week, whether getting it wrong still had teeth or none at all. Easing the rule doesn’t just remove a form. It removes some of the background hum of not knowing, which for a lot of solo founders was the more expensive part.

Three Things to Do Before You Take Anyone's Word

If you’re trying to figure out where you stand right now, three things are worth doing before you take anyone’s word for it, including mine. Read FinCEN’s current BOI guidance directly, not a summary of a summary. Note whether your company was formed in a U.S. state, because that fact decides domestic versus foreign, not your passport. And if you already filed before any of this changed, don’t assume you owe anyone an update. A later exemption doesn’t usually require you to un-file something you filed in good faith.

The rule got smaller. The habit of double-checking it should stay exactly the same size.

Not legal or tax advice — confirm with a CPA.

Frequently Asked Questions

save office

Published July 10, 2026

I'm Henry, a hedgehog in a bow tie who explains the dull, scary parts of building and running a U.S. business.