Key takeaways

- US business credit is built through DUNS (Dun & Bradstreet) registration plus accounts with Net 30 vendors that report to credit bureaus.

- Address consistency matters; D&B verifies the address against state SOS records and rejects applications with mismatches.

- Most founders skip business credit entirely; it becomes relevant only when applying for SBA loans, large vendor accounts, or commercial leases.

Before you start

- Confirm the LLC's address is identical across the state SOS filing, EIN letter, and any commercial register.

- Identify which Net 30 vendors report to D&B, Experian Business, and Equifax Business.

Who this is for

- LLC owners planning to apply for SBA loans or commercial leases in Year 2-3.

- Operators sourcing inventory or services that require business credit.

Building business credit is a separate financial track from personal credit, with separate scores, separate bureaus, and separate verification rules. Done right, an LLC owner ends up with a credit profile that lets the business borrow, get vendor terms, and qualify for a no-personal-guarantee credit card without putting the owner's personal score at risk.

The full process takes about six months and follows a five-step ladder: form the LLC and get an EIN, register a DUNS number with Dun & Bradstreet, open Net 30 vendor accounts that report to the bureaus, add a business credit card, and monitor and grow the resulting credit profile. Each step has its own gotchas, and the most common failure point across all five steps is the address.

D&B, Experian Business, and Equifax Business all verify that the LLC operates at a real commercial location. A home address, an apartment, a residential mailbox rental, or a PO Box fails that verification. The fix is a commercial business address with documentation: a lease agreement or a license agreement from a virtual office provider with a USPS commercial classification. This guide covers the full ladder, the address rule at each step, and how to put the documentation together before the first application goes in.

Setting up your LLC? See your US address options — no card →

Why business credit is separate from personal credit

Personal credit reports run through Experian, Equifax, and TransUnion under the FCRA. Business credit reports run through D&B, Experian Business, and Equifax Business under different reporting rules. The two systems share almost nothing: they pull from different data sources, use different scoring models, and follow different dispute processes.

The biggest practical difference is the scoring scale. Personal FICO scores run 300 to 850. The D&B PAYDEX score runs 1 to 100, with 80+ considered prime. Experian Intelliscore Plus runs 1 to 100 in V1 and V2 (the versions most lenders still use); the newer V3 expanded to 300 to 850. Equifax Business Credit Risk Score runs 101 to 992. A business owner who has perfect personal credit can have no business credit profile at all, since the two systems track entirely separate accounts.

- Personal credit (FICO). Pulls from credit cards, mortgages, auto loans, and student loans reported under the owner's SSN. Affects personal lending and rental applications.

- Business credit (PAYDEX, Intelliscore, Equifax Business). Pulls from vendor accounts, business credit cards, and business loans reported under the LLC's EIN and DUNS number. Affects business lending, vendor terms, and supplier limits.

- The crossover risk. A personal guarantee on a business card makes the business debt show up on the personal credit report too. Avoiding the personal guarantee is the second goal of building business credit, after growing the score itself.

Why most founders skip business credit entirely

The personal-guarantee shortcut works for the first card or two, but it caps how much an LLC can borrow before the personal score becomes the bottleneck. Business credit unlocks higher limits without the personal guarantee, which matters as the LLC scales past the $50K-$100K monthly revenue mark.

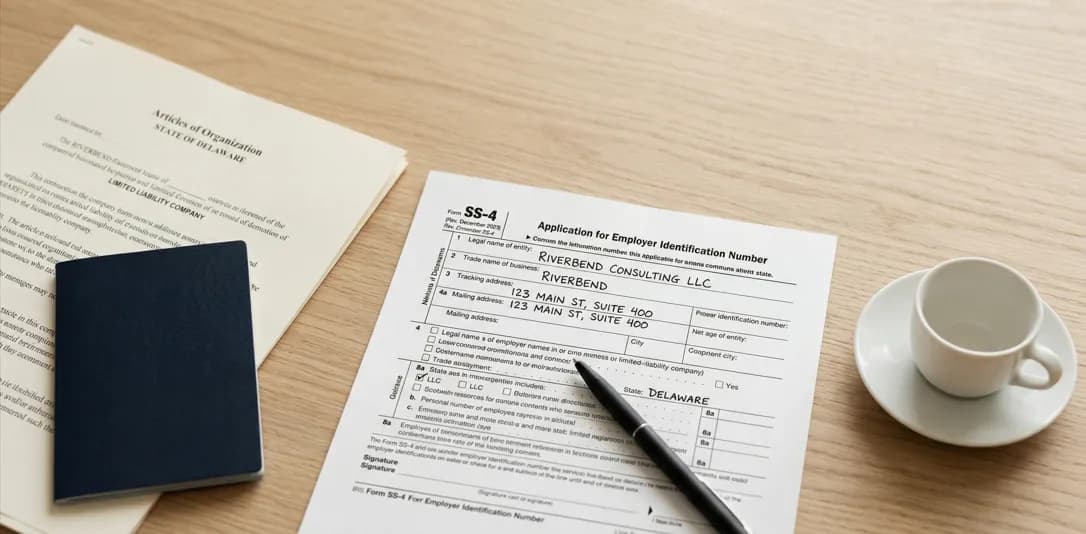

Step 1: Form the LLC and get the EIN

The foundation for business credit is an LLC (or corporation) that the bureaus can identify as a separate entity from the owner. Sole proprietorships and DBAs generally struggle to build a separate business credit profile because they share the owner's SSN with the IRS. The legal entity needs to be the borrower of record on every account that reports.

- 1File the Articles of Organization with a state Secretary of State. The state filing creates the LLC and assigns it a state file number. Total cost ranges from $35 (Montana, the lowest nationwide) to $500 (Massachusetts), with most states between $100 and $200.

- 2Get an EIN from the IRS using Form SS-4. The EIN is the LLC's federal tax ID, and it is also what the credit bureaus use to identify the entity. Foreign founders without an SSN can apply for an EIN by mail or fax through the IRS International Department, with detail in the companion guide on EIN without SSN.

- 3Open a business bank account in the LLC's name using the EIN and Articles. The bank account creates a financial transaction history that the bureaus eventually use as additional data, and it separates the LLC's finances from the owner's personal accounts. The business bank account address requirements guide covers the address documentation banks ask for during onboarding.

- 4File a fictitious business name (DBA) if the LLC operates under a name different from its legal name. Some lenders use the DBA as the public-facing name on the credit profile. Most LLCs do not need a DBA at this step, but check the operating state's rules if the LLC plans to do business under multiple brands.

Address consistency matters across every record

The address used on the Articles, the EIN application, the bank account, and every credit application has to match exactly. The credit bureaus run automated address-matching against the IRS records and the state Secretary of State records, and any mismatch flags the application for manual review. Use the same business address from day one, and update all four (state, IRS Form 8822-B, bank, and any vendor accounts) together if the address ever changes.

Ready to set up your business address?

See which US cities fit — about a minute, no card needed.

Step 2: Get a DUNS number and pass the D&B address verification

The DUNS number is a nine-digit business identifier issued by Dun & Bradstreet, one of the oldest and most widely-used business credit bureaus. A DUNS number is free, takes up to 30 business days to process for a new entity, and is the prerequisite for the D&B PAYDEX score that most vendors and lenders check before extending credit.

- 1Apply at the D&B website using the LLC's legal name, EIN, business address, and a phone number where someone can answer during business hours. The application asks for the year the business started (use the LLC formation date), the number of employees, and the SIC industry code.

- 2Wait up to 30 business days for processing. D&B does not publish what it checks. Its own page says only that you 'may be contacted by a representative of Dun & Bradstreet to validate your information.' What follows below is what applicants commonly report, not a published rule. A paid expedited option delivers within eight business days; D&B does not publish the price on that page.

- 3Confirm the entry in the D&B database. Once approved, the LLC has a DUNS number visible at the D&B Direct lookup tool. The PAYDEX score is unscored until D&B receives payment data from at least two reporting vendors with three trade experiences; once enough trade history is reported, the score appears on a 1-100 scale.

The D&B address verification step

D&B specifically checks that the address on the DUNS application is a commercial business address that matches the address the LLC filed with the IRS and the Secretary of State. Applicants commonly report a USPS commercial classification check and sometimes a phone call to the address. A PO Box is not a deliverable street address for verification mail. A virtual office or executive suite that is USPS-classified as commercial gives the reviewer a commercial street address and a suite, which is what the application asks for. D&B decides the rest.

The address rule is where most founders without a commercial location get stuck. The fix is straightforward: secure a real commercial business address with a lease or license agreement before applying for the DUNS number. The agreement does not need to be a full office lease. A virtual office license agreement from a USPS commercial-classified provider gives D&B the same two documents a coworking license or a small office lease would: a commercial classification and an agreement naming the applicant.

save office operates commercial-classified addresses across six US cities (New York, San Francisco, Wilmington Delaware, Cheyenne Wyoming, Tampa Florida, and Washington DC) with a license agreement on file from day one. The address activates within 24 hours, which means the DUNS application can be submitted the same week the LLC files its Articles. The address-checker tool flags whether a current or proposed address has the commercial USPS classification that D&B looks for.

Step 3: Open Net 30 vendor accounts that report to the bureaus

The PAYDEX score grows when vendors and creditors report payment history to D&B. Most consumer-facing vendors do not report business credit. The vendors that report are a specific list of suppliers and trade creditors that participate in the D&B Trade Exchange or its Experian and Equifax equivalents.

| Vendor | What it reports | Sign-up requirements | Notes |

|---|---|---|---|

| Uline | PAYDEX (D&B), Experian Business | DUNS number, business email, business phone, EIN | Largest reporting Net 30 vendor; ships from regional warehouses; minimum order around $50 |

| Quill | PAYDEX (D&B), Experian Business | DUNS number, business address, EIN | Office and shipping supplies; Net 30 terms approved automatically for most LLCs after the first order |

| Grainger | PAYDEX, Experian Business, Equifax Business | DUNS number, business address, business phone | Industrial supplies; reports to all three bureaus; Net 30 terms after credit application |

| Crown Office Supplies | PAYDEX (D&B) | DUNS number, business email, EIN | Office supplies; lower minimum than Uline; faster Net 30 approval for new LLCs |

| Summa Office Supplies | PAYDEX, Experian Business | DUNS number, business address, EIN | Office supplies; one of the few Net 30 accounts that explicitly accepts businesses with limited credit history |

| JJ Gold International | PAYDEX (D&B) | DUNS number, business email, EIN | Wholesale jewelry and gifts; useful for retailers and resellers, less useful for service businesses |

Common Net 30 vendors that report to the major business credit bureaus. Reporting frequency is monthly. Always confirm reporting status with the vendor before applying, since reporting policies change.

The strategy is to open three to five reporting Net 30 accounts in the first three months, place small recurring orders to generate payment history, and pay every invoice on or before the due date. PAYDEX scoring rewards early payment: paying 30 days early earns the maximum 100, paying on the due date earns 80, and paying 30 days late typically drops the score into the 50-79 range. Most lenders want PAYDEX 80+ for unsecured business credit lines.

The address rule for Net 30 vendors

Several Net 30 vendors run their own commercial-classification check before approving a Net 30 account. Uline and Grainger generally favor commercial shipping addresses, and applications from residential addresses may receive additional manual review. Quill is more flexible but still verifies the EIN and business address against the IRS records. The same commercial address that passed the DUNS verification typically passes the Net 30 vendor verification.

save office's license agreement specifically names the LLC as the licensee, which is the document the Net 30 vendor underwriting team asks for when an application gets flagged for additional review. A USPS commercial classification, a license agreement on file, and an active DUNS number are the documentation set the underwriting team usually asks for. What the vendor does with it is the vendor's decision.

Step 4: Add a business credit card without a personal guarantee

After three to four months of Net 30 vendor reporting and a PAYDEX score in the 70-80 range, the LLC qualifies for a business credit card. Most issuers require a personal guarantee for new businesses, but a few cards are available without one. The trade-off is that no-personal-guarantee cards usually require revenue history, a longer time-in-business, or a higher D&B score.

- Brex. No personal guarantee. Funded startups typically need around $50K in a connected business bank account; commercial businesses generally need over $1M in annual revenue. Reports to D&B and Experian Business. Available to LLCs with a US business bank account and EIN. Foreign founders without SSN are eligible if the LLC has US revenue. (Capital One's acquisition of Brex closed in April 2026, so underwriting criteria may continue to shift.)

- Ramp. No personal guarantee. Generally requires at least $25K in a US business bank account balance. Reports to D&B. Card limits adjust based on the LLC's bank account balance. Strong fit for LLCs that have been running 6-12 months with steady revenue.

- Capital One Spark Cash Plus. Requires a personal guarantee but reports business activity, not personal. Useful as a starter card for LLCs that have not yet hit the Brex or Ramp thresholds.

- American Express Business. Requires a personal guarantee for most cards. Reports to D&B Premier and Experian Business. Higher reporting weight than most other issuers, which makes it a strong choice for the second card on the credit profile.

The path most founders take

Start with a personal-guarantee card (Capital One Spark or Amex Business) for the first 6-12 months, build the PAYDEX score and revenue history, then upgrade to Brex or Ramp once the LLC qualifies for the no-personal-guarantee tier. The personal guarantee on the first card limits to a few thousand dollars of personal exposure, which is reversible once the upgrade happens and the original card is closed.

Step 5: Monitor and grow the credit profile

Once the DUNS number is active, the Net 30 accounts are reporting, and the credit card is open, the LLC has a credit profile. Monitoring keeps the profile clean and catches reporting errors early. Growing the profile means adding more reporting accounts, holding lower utilization, and avoiding late payments.

- D&B PAYDEX. 80+ is prime. Monitor at the D&B Credit Insights dashboard ($49/month for the Basic tier; $149/month for Plus). Free alternatives include the iUpdate portal for self-corrections and the D&B Direct API tier for high-volume monitoring.

- Experian Business Intelliscore Plus. 76+ is low risk. Monitor at the Experian Business credit dashboard ($39/month). The Smart Business Reports plan includes alerts for changes.

- Equifax Business Credit Risk Score. The scale runs 101 to 992; a higher score typically indicates lower risk. Specific cutoffs vary by lender. Equifax does not offer a self-monitoring product comparable to D&B or Experian; lenders pull the report directly when needed.

- Annual review of all three reports. Errors are common, especially address mismatches and account-level reporting gaps. Disputes go through each bureau separately, and a clean dispute usually resolves within 30 days.

After 12 months of consistent reporting, an LLC with PAYDEX 80+ and Intelliscore 76+ qualifies for unsecured business lines of credit, larger Net 30 limits with major suppliers, and lower deposits on commercial leases and utility accounts. The credit profile becomes a long-term asset that compounds with each additional reporting account.

The address rule across the credit-building stack

Every step of the business credit ladder runs through the same address verification system. The bureaus, the vendors, and the issuers all check whether the LLC operates at a real commercial location. The check is automated for most applications and manual for flagged applications. The same address has to work across every step.

| Verifier | What gets checked | Pass criteria | Common fail |

|---|---|---|---|

| D&B (DUNS) | USPS commercial classification + IRS/SOS match | Commercial-classified address with lease or license agreement | Residential address, PO Box, mismatch with state filing |

| Net 30 vendors (Uline, Grainger) | Commercial classification + phone verification | Commercial address with answerable business phone | Residential ZIP, address shows as apartment or house |

| Business banks (Mercury, Brex Treasury, Chase) | KYB verification + address match with IRS records | Address that matches Articles + EIN application | Address inconsistency across documents |

| Stripe and PayPal | Address verification + business documentation | Commercial address with business operations evidence | Residential address triggers manual review |

| Credit card issuers (Brex, Ramp, Amex) | Combined personal + business credit pull | Established commercial address + active reporting accounts | New address with no history |

Address verification across the major points in the business credit stack. The same commercial address passes all five if it is USPS-classified as commercial, has a lease or license on file, and matches the address on the IRS EIN records.

The six-city table below lists the save office locations and the documentation each one carries into these verification layers. What a bureau does with that documentation is its decision, and we do not publish an approval rate, because we do not have one. Each address has a license agreement on file with the LLC as the licensee and a USPS commercial classification. One note on the phone line: save office provides the address, not a phone service, so the answerable business phone that Net 30 vendors check is something to set up separately. The 24-hour activation means the DUNS application can be submitted within a week of LLC formation, and the full credit-building ladder can complete in six months from formation.

| City | USPS class | License doc | Activation | Best fit |

|---|---|---|---|---|

| New York | Commercial | License agreement | 24 hours | Northeast clients and finance-sector credit profile |

| San Francisco | Commercial | License agreement | 24 hours | Tech and startup vendor accounts (Brex, Mercury, Ramp HQ) |

| Wilmington Delaware | Commercial | License agreement | 24 hours | Delaware-formed LLCs needing a real principal address |

| Cheyenne Wyoming | Commercial | License agreement | 24 hours | Wyoming-formed LLCs and lowest annual fees |

| Tampa Florida | Commercial | License agreement | 24 hours | Florida operations, no state income tax |

| Washington DC | Commercial | License agreement | 24 hours | Government-adjacent contracts and biennial-only reporting |

save office locations, the USPS classification each one carries, and the license agreement available from day one. Approval is the reviewing bureau's decision, not a property of the address.

Where save office fits the business credit ladder

A real commercial business address is the foundation that the rest of the credit ladder runs on. Without one, applications across DUNS, Net 30 vendors, and business banking often face additional scrutiny or manual review. A clean commercial address generally helps each step move forward without delays.

save office provides the commercial-classified address with a license agreement and the 24-hour activation that fits the timeline of building business credit from LLC formation. A phone line is not part of the service, so plan for that separately. The companion guide on the three business addresses every LLC needs covers how the principal business address, the registered agent address, and the mailing address fit together. The address-checker tool checks whether a proposed address passes the USPS commercial classification check that D&B and Net 30 vendors run.

Frequently Asked Questions

Not sure what you need?

Two short pages sort it out — what the products actually are, and which situation you're in.